下单交易

创建订单

对应的请求类:TradeOrderRequest

说明

交易下单接口。关于如何选择标的、订单类型、方向数量等,请见下方说明。请在运行程序前结合本文档的概述部分及FAQ-交易-支持的订单列表部分,检查您的账户是否支持所请求的订单,并检查交易规则是否允许在程序运行时段对特定标的下单。若下单失败,可首先阅读文档FAQ-交易部分排查

CAUTION

1、市价单(MKT)和止损单(STP)不支持盘前盘后阶段交易,在调用下单接口时,需要把 outside_rth 设置为 false

2、对于可做空标的,暂不支持锁仓功能,因此无法同时持有相同标的多头和空头持仓

3、附加订单的主订单类型暂时仅支持限价单

4、限价价格不匹配tickSize,可以参考合约返回tickSizes字段,利用StockPriceUtils工具类判断是否匹配,修复价格符合tickSize要求

5、市价单(MKT)和模拟账号,对'time_in_force'参数都不支持GTC

6、模拟账号暂不支持窝轮和牛熊证的订单

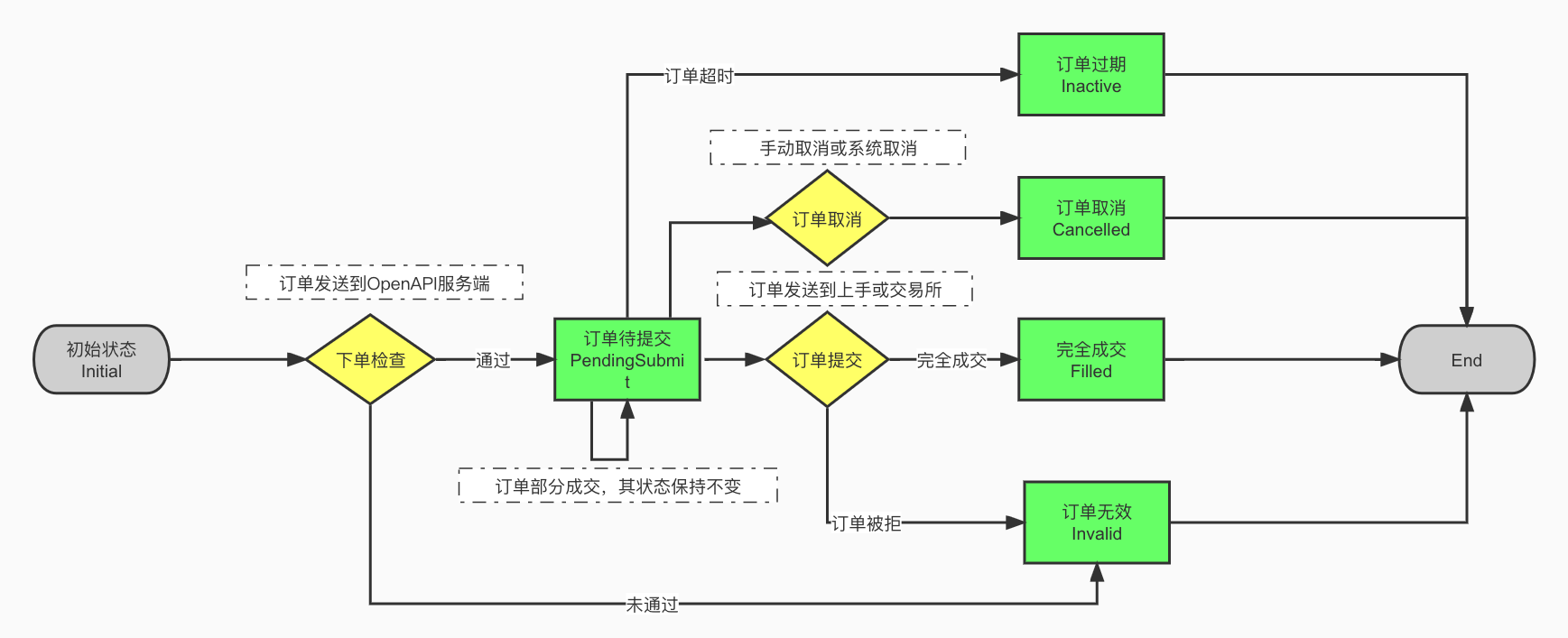

订单状态说明

如何判断综合和模拟账号的部分成交状态?

当订单状态不是Initial和Filled(有可能是PendingSubmit,Cancelled,Invalid,Inactive其中一种)时,都有可能是部分成交的状态,可以通过订单成交数量是否大于0来判断

如何判断环球账号部分成交状态?

订单状态是 Filled,且订单成交数量大于0

订单状态变化流程:

其他说明

- 指数期权除 IWM/SPY/QQQ 外, 不支持非周五期权的交易

- 不可以直接开反向仓位,如持仓100股,直接卖出200股是不允许的,需先平仓

参数

| 参数 | 类型 | 描述 | 市价单 | 限价单 | 止损单 | 止损限价单 | 跟踪止损单 |

|---|---|---|---|---|---|---|---|

| account | string | 用户授权账户:402901 | |||||

| order_id | int | 订单编号,作用是防止重复下单。可以通过订单号接口获取。如果传0,则服务器端会自动生成订单编号,传0时无法防止重复下单,请谨慎选择 | 选填 | 选填 | 选填 | 选填 | 选填 |

| symbol | string | 股票代码 如:AAPL;(sec_typ为窝轮牛熊证时,在app窝轮/牛熊证列表中名称下面的5位数字) | |||||

| sec_type | string | 合约类型 (STK 股票;OPT 美股期权; WAR 港股窝轮; IOPT 港股牛熊证; FUT 期货; FUND 基金) | |||||

| action | string | 交易方向 BUY/SELL | |||||

| order_type | string | 订单类型. MKT(市价单), LMT(限价单), STP(止损单), STP_LMT(止损限价单), TRAIL(跟踪止损单) | MKT | LMT | STP | STP_LMT | TRAIL |

| total_quantity | long | 下单数量(港股,沪港通,窝轮,牛熊证有最小数量限制) | |||||

| total_quantity_scale | int | 下单数量的偏移量,默认为0。碎股单的total_quantity 和 total_quantity_scale 结合起来代表真实下单数量,如 total_quantity=111 total_quantity_scale=2,那么真实 quantity=111*10^(-2)=1.11 | 选填 | 选填 | 选填 | 选填 | 选填 |

| cash_amount | Double | 订单金额(基金等金额订单) | 选填 | ||||

| limit_price | double | 限价,当 order_type 为LMT,STP_LMT时该参数必需 | |||||

| aux_price | double | 股票订单止损触发价。含义为价差,与trailing_percent同时存在时被trailing_percent覆盖。当 order_type 为STP,STP_LMT时该参数必需,当 order_type 为 TRAIL时,为跟踪额 | 选填 | ||||

| trailing_percent | double | 跟踪止损单-止损百分比 。当 order_type 为 TRAIL时,aux_price和trailing_percent两者互斥,优先使用trailing_percent | 选填 | ||||

| outside_rth | boolean | true: 允许盘前盘后交易(美股专属), false: 不允许,默认为允许。(市价单、止损单、跟踪止损单只在盘中有效,将忽略outside_rth参数) | 选填 | 选填 | 选填 | ||

| trading_session_type | TradingSessionType | 美股订单时段(仅限价单)。枚举值详见: 订单时段枚举 | 选填 | 选填 | |||

| adjust_limit | double | 价格微调幅度(默认为0表示不调整,正数为向上调整,负数向下调整),对传入价格自动调整到合法价位上。例如:0.001 代表向上调整且幅度不超过 0.1%;-0.001 代表向下调整且幅度不超过 0.1%。默认 0 表示不调整 | 选填 | 选填 | 选填 | 选填 | |

| market | string | 市场 (美股 US 港股 HK 沪港通 CN) | 选填 | 选填 | 选填 | 选填 | 选填 |

| currency | string | 货币(美股 USD 港股 HKD 沪港通 CNH) | 选填 | 选填 | 选填 | 选填 | 选填 |

| time_in_force | string | 订单有效期,只能是 DAY(当日有效)、GTC(取消前有效,最长有效时间180天)、GTD(在指定时间前有效),默认为DAY | 选填 | 选填 | 选填 | 选填 | 选填 |

| expire_time | long | 订单有效的截止时间, 13位的时间戳,精确到秒(time_in_force为GTD时为必填,其他类型时无效) | 选填 | 选填 | 选填 | ||

| exchange | string | 交易所 (美股 SMART 港股 SEHK 沪港通 SEHKNTL 深港通 SEHKSZSE)否 | 选填 | 选填 | 选填 | 选填 | 选填 |

| expiry | string | 过期日(期权、窝轮、牛熊证专属) | 选填 | 选填 | 选填 | 选填 | 选填 |

| strike | string | 底层价格(期权、窝轮、牛熊证专属) | 选填 | 选填 | 选填 | 选填 | 选填 |

| right | string | 期权方向 PUT/CALL(期权、窝轮、牛熊证专属) | 选填 | 选填 | 选填 | 选填 | 选填 |

| multiplier | float | 1手单位(期权、窝轮、牛熊证专属) | 选填 | 选填 | 选填 | 选填 | 选填 |

| local_symbol | string | 窝轮牛熊证该字段必填,在app窝轮/牛熊证列表中名称下面的5位数字 | 选填 | 选填 | 选填 | 选填 | 选填 |

| secret_key | string | 机构用户专用,交易员密钥 | 选填 | 选填 | 选填 | 选填 | 选填 |

| user_mark | String | 下单备注信息,下单后不能修改,查询订单时返回userMark信息 | 选填 | 选填 | 选填 | 选填 | 选填 |

- 附加订单参数

附加订单(Attached Order )是指能通过附加的子订单对主订单起到止盈或止损效果的订单,可以附加的子订单类型有限价单(可用于止盈)、止损限价单/止损单(可用于止损)。通过增加以下参数可以实现附加订单

| 参数 | 类型 | 描述 | 附加止损 | 附加止盈 | 附加跟踪止损 | 附加括号 |

|---|---|---|---|---|---|---|

| attach_type | string | 附加订单类型,下附加订单时必填。(order_type应为LMT): PROFIT-止盈单,LOSS-止损单,BRACKETS-括号订单(包含附加止盈单和附加止损单) | ||||

| profit_taker_orderId | int | 止盈单编号,可以通过订单号接口获取。如果传0,则服务器端会自动生成止盈单编号 | 选填 | 选填 | 选填 | |

| profit_taker_price | double | 止盈单价格,下止盈单时必填 | ||||

| profit_taker_tif | string | 同time_in_force字段,订单有效期,只能是 DAY(当日有效)和GTC(取消前有效),下止盈单时必填 | ||||

| profit_taker_rth | boolean | 同outside_rth字段 | ||||

| stop_loss_orderId | int | 止损单编号,可以通过订单号接口获取。如果传0,则服务器端会自动生成止损单编号 | ||||

| stop_loss_price | double | 止损单价格(止损单的触发价),下止损单时必填 | ||||

| stop_loss_limit_price | double | 止损单的执行限价(暂只对综合账号有效)。止损单的限价没有填写时,为附加止损市价单 | 选填 | 选填 | ||

| stop_loss_tif | string | 同time_in_force字段,订单有效期,只能是 DAY(当日有效)和GTC(取消前有效),下止损单时必填 | ||||

| stop_loss_trailing_percent | double | 跟踪止损单-止损百分比,当下跟踪止损单时,止损百分比(stopLossTrailingPercent)和止损额(stopLossTrailingAmount)其中一项必填,如果都填时,会使用止损百分比作为参数。 | 选填 | 选填 | ||

| stop_loss_trailing_amount | double | 跟踪止损单-止损额,当下跟踪止损单时,止损百分比(stopLossTrailingPercent)和止损额(stopLossTrailingAmount)其中一项必填,如果都填时,会使用止损百分比作为参数。 | 选填 | 选填 |

- TWAP/VWAP订单参数

TWAP/VWAP订单,只支持美股股票标的,只能在盘中下单,不支持预挂单

| 参数 | 类型 | 算法参数 | 描述 | TWAP | VWAP |

|---|---|---|---|---|---|

| order_type | string | 订单类型,TWAP/VWAP | |||

| account | string | 资金账号 | |||

| symbol | string | 股票代码 如:AAPL | |||

| sec_type | string | 只支持STK | |||

| total_quantity | boolean | 订单数量 | |||

| algo_params | List<TagValue> | 算法参数 | 选填 | 选填 | |

| - | long | start_time | 策略开始时间(时间戳) | 选填 | 选填 |

| - | long | end_time | 策略结束时间(时间戳) | 选填 | 选填 |

| - | string | participation_rate | 最大参与率(成交量为日均成交量的最大比例,0.01-0.5) | 选填 |

返回

| 名称 | 类型 | 说明 |

|---|---|---|

| id | long | 唯一单号ID,可用于查询订单/修改订单/取消订单 |

| subIds | List<Long> | 附加单时,返回子订单号ID列表 |

| orders | List<TradeOrder> | 返回订单详细信息 |

构建合约对象

// 美股股票合约

ContractItem contract = ContractItem.buildStockContract("SPY", "USD");

// 港股股票合约

ContractItem contract = ContractItem.buildStockContract("00700", "HKD");

// 港股窝轮合约(需要注意同一个symbol,环球账号和综合账号的expiry可能不同)

ContractItem contract = ContractItem.buildWarrantContract("13745", "20211217", 719.38D, Right.CALL.name());

// 港股牛熊证合约

ContractItem contract = ContractItem.buildCbbcContract("50296", "20220331", 457D, Right.CALL.name());

// 美股期权合约

ContractItem contract = ContractItem.buildOptionContract("AAPL 190118P00160000");

ContractItem contract = ContractItem.buildOptionContract("AAPL", "20211119", 150.0D, "CALL");

// 期货合约

// 环球账户

ContractItem contract = ContractItem.buildFutureContract("CL", "USD", "SGX", "20190328", 1.0D);

// 综合账户

ContractItem contract = ContractItem.buildFutureContract("CL2112", "USD");

市价单(MKT)

// get contract(use default account)

ContractRequest contractRequest = ContractRequest.newRequest(new ContractModel("AAPL"));

ContractResponse contractResponse = client.execute(contractRequest);

ContractItem contract = contractResponse.getItem();

// market order(use default account)

TradeOrderRequest request = TradeOrderRequest.buildMarketOrder(contract, ActionType.BUY, 10);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// get contract(use account parameter)

ContractRequest contractRequest = ContractRequest.newRequest(new ContractModel("AAPL"), "402901");

ContractResponse contractResponse = client.execute(contractRequest);

ContractItem contract = contractResponse.getItem();

// market order(use account parameter)

request = TradeOrderRequest.buildMarketOrder("402901", contract, ActionType.BUY, 10);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

限价单(LMT)

// use default account

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder(contract, ActionType.BUY, 1, 100.0d);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 100.0d);

// set user_mark

request.setUserMark("test001");

// set GTD order's expire_time

request.setTimeInForce(TimeInForce.GTD);

request.setExpireTime(1669363583804L);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

夜盘/ 全时段订单(overnight/full-time)

// place overnight order in the US market

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 200.0d);

request.setTradingSessionType(TradingSessionType.OVERNIGHT);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// place full-time order in the US market

request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 200.0d);

request.setTradingSessionType(TradingSessionType.FULL);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

竞价单(AM/AL)

// auction order in hk market

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 100, 100.0d);

// 盘前竞价: AM or AL + OPG, 如果未成交参与盘中交易; 盘后竞价: AM or AL + DAY

// participate in the pre-market auction, set auction limit order

request.setAuctionOrder(OrderType.AL, TimeInForce.OPG);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

request = TradeOrderRequest.buildMarketOrder("402901", contract, ActionType.BUY, 100);

// Participate in the after-hours auction, set auction market order

request.setAuctionOrder(OrderType.AM, TimeInForce.OPG);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

止损单(STP)

// use default account

TradeOrderRequest request = TradeOrderRequest.buildStopOrder(contract, ActionType.BUY, 1, 120.0d);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildStopOrder("402901", contract, ActionType.BUY, 1, 120.0d);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

止损限价单(STP_LMT)

// use default account

TradeOrderRequest request = TradeOrderRequest.buildStopLimitOrder(contract, ActionType.BUY, 1,150d,130.0d);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildStopLimitOrder("402901", contract, ActionType.BUY, 1,150d,130.0d);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

跟踪止损单(TRAIL)

// use default account

TradeOrderRequest request = TradeOrderRequest.buildTrailOrder(contract, ActionType.BUY, 1,10d,130.0d);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter. standard account currently not supported

request = TradeOrderRequest.buildTrailOrder("402901", contract, ActionType.BUY, 1, 10d, 130.0d);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

主订单+附加止盈单

// use default account

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder(contract, ActionType.BUY, 1, 199d);

TradeOrderRequest.addProfitTakerOrder(request, 250D, TimeInForce.DAY, Boolean.FALSE);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 199d);

TradeOrderRequest.addProfitTakerOrder(request, 250D, TimeInForce.DAY, Boolean.FALSE);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

主订单+附加止损单

// use default account

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder(contract, ActionType.BUY, 1, 129d);

TradeOrderRequest.addStopLossOrder(request, 100D, TimeInForce.DAY);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 129d);

// 添加附加止损市价单,附加止损价格是触发价(不支持期权标的)

TradeOrderRequest.addStopLossOrder(request, 100D, TimeInForce.DAY);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// 期权可以使用附加止损限价单

ContractItem optionContract = ContractItem.buildOptionContract("AAPL", "20211231", 175.0D, "CALL");

request = TradeOrderRequest.buildLimitOrder("402901", optionContract, ActionType.BUY, 1, 2.0d);

// 添加附加止损限价单,其中第一个价格1.7是触发价,第二个价格1.69是附加止损单的挂单限价(暂只支持综合账号)

TradeOrderRequest.addStopLossLimitOrder(request, 1.7D, 1.69D, TimeInForce.DAY);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

主订单+附加跟踪止损单

ContractItem contract = ContractItem.buildStockContract("AAPL", "USD");

// use default account

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder(contract, ActionType.BUY, 1, 165D);

TradeOrderRequest.addStopLossTrailOrder(request, 10.0D, null, TimeInForce.DAY);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildLimitOrder("402901", contract, ActionType.BUY, 1, 165D);

TradeOrderRequest.addStopLossTrailOrder(request, 10.0D, null, TimeInForce.DAY);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

主订单+附加括号订单

// use default account

TradeOrderRequest request = TradeOrderRequest.buildLimitOrder(contract, ActionType.BUY, 1, 199d);

TradeOrderRequest.addBracketsOrder(request, 250D, TimeInForce.DAY, Boolean.FALSE, 180D, TimeInForce.GTC);

TradeOrderResponse response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

// use account parameter

request = TradeOrderRequest.buildLimitOrder("13810712", contract, ActionType.BUY, 1, 199d);

TradeOrderRequest.addBracketsOrder(request, 250D, TimeInForce.DAY, Boolean.FALSE, 180D, TimeInForce.GTC);

response = client.execute(request);

System.out.println(JSONObject.toJSONString(response));

换汇单

ForexTradeOrderRequest request = ForexTradeOrderRequest.buildRequest("402901",

SegmentType.SEC, Currency.HKD, 1000D, Currency.USD);

ForexTradeOrderResponse response = client.execute(request);

if (response.isSuccess()) {

System.out.println(JSONObject.toJSONString(response));

} else {

System.out.println(response.getMessage());

}

基金金额单

ContractItem contract = ContractItem.buildFundContract("IE00B464Q616.USD", "USD");

TradeOrderRequest request = TradeOrderRequest.buildAmountOrder(

"13810712", contract, ActionType.BUY, 100.0D);

request.setUserMark("test-amount-order");

TradeOrderResponse response = client.execute(request);

if (response.isSuccess()) {

System.out.println(JSONObject.toJSONString(response));

} else {

System.out.println(response.getMessage());

}

TWAP/VWAP订单

只支持美股股票,只支持盘中下单。不能改单,可以撤单

// TWAP order

TradeOrderRequest twapRequest = TradeOrderRequest.buildTWAPOrder(

"572386", "DM", ActionType.BUY, 500,

DateUtils.getTimestamp("2023-06-20 09:30:00", TimeZoneId.NewYork),

DateUtils.getTimestamp("2023-06-20 11:00:00", TimeZoneId.NewYork),

1.5D)

.setUserMark("testTWAP001")

.setLang(Language.en_US);

TradeOrderResponse twapResponse = client.execute(twapRequest);

if (twapResponse.isSuccess()) {

System.out.println(JSONObject.toJSONString(twapResponse));

} else {

System.out.println(twapResponse.getMessage());

}

// VWAP order

TradeOrderRequest vwapRequest = TradeOrderRequest.buildVWAPOrder(

"572386", "DM", ActionType.BUY, 500,

DateUtils.getTimestamp("2023-06-20 09:30:00", TimeZoneId.NewYork),

DateUtils.getTimestamp("2023-06-20 11:00:00", TimeZoneId.NewYork),

0.5D, 1.5D)

.setUserMark("testVWAP001")

.setLang(Language.en_US);

TradeOrderResponse vwapResponse = client.execute(vwapRequest);

if (vwapResponse.isSuccess()) {

System.out.println(JSONObject.toJSONString(vwapResponse));

} else {

System.out.println(vwapResponse.getMessage());

}

期权多腿订单

只支持盘中下单

List<ContractLeg> contractLegs = new ArrayList<>();

ContractLeg leg1 = new ContractLeg(SecType.OPT, "AAPL",

"170.0", "20231013", Right.CALL,

ActionType.BUY, 1);

contractLegs.add(leg1);

ContractLeg leg2 = new ContractLeg(SecType.OPT, "AAPL",

"170.0", "20231013", Right.PUT,

ActionType.BUY, 1);

contractLegs.add(leg2);

TradeOrderRequest request = TradeOrderRequest.buildMultiLegOrder(

"572386", contractLegs, ComboType.CUSTOM,

ActionType.BUY, 3,

OrderType.LMT, 2.01d, null, null)

.setLang(Language.en_US)

.setUserMark("test_multi_leg");

TradeOrderResponse response = client.execute(request);

if (response.isSuccess()) {

System.out.println(JSONObject.toJSONString(response));

} else {

System.out.println(response.getMessage());

}

OCA括号单

OCA括号订单内的两个订单标的相同,一个止盈限价单,另一个为止损单或者止损限价单。其中一个成交时,自动取消另一个订单。下单后返回两个order对象,订单中的'ocaGroupId'相同的为一个组合。 不支持模拟盘

ContractItem contract = ContractItem.buildStockContract("BILI", "USD");

TradeOrderRequest request = TradeOrderRequest.buildOCABracketsOrder(

"13810712", contract, ActionType.SELL, 1,

17.0D, TimeInForce.DAY, Boolean.TRUE,

12.0D, null, TimeInForce.DAY, Boolean.FALSE);

request.setLang(Language.en_US).setUserMark("test-oca");

TradeOrderResponse response = client.execute(request);

if (response.isSuccess()) {

System.out.println(JSONObject.toJSONString(response));

// get oca order info

List<TradeOrder> ocaOrders = response.getItem().getOrders();

} else {

System.out.println(response.getMessage());

}

返回示例 附加括号单

{

"id":30325712346546176,

"orderId":0,

"subIds":[

30325712346546177,

30325712346677250

],

"orders":[

{

"account":"13810712",

"action":"BUY",

"algoStrategy":"LMT",

"attrDesc":"",

"avgFillPrice":0,

"canCancel":true,

"canModify":true,

"commission":0,

"currency":"HKD",

"discount":0,

"filledQuantity":0,

"id":30325712346546176,

"identifier":"00700",

"latestPrice":385.8,

"latestTime":1680266023000,

"limitPrice":295,

"liquidation":false,

"market":"HK",

"name":"腾讯控股",

"openTime":1680266023000,

"orderId":91,

"orderType":"LMT",

"outsideRth":true,

"realizedPnl":0,

"remark":"",

"secType":"STK",

"source":"OpenApi",

"status":"Initial",

"symbol":"00700",

"timeInForce":"DAY",

"totalQuantity":100,

"updateTime":1680266023000,

"userMark":"test_bracket"

},

{

"account":"13810712",

"action":"SELL",

"algoStrategy":"LMT",

"attrDesc":"",

"avgFillPrice":0,

"canCancel":true,

"canModify":true,

"commission":0,

"currency":"HKD",

"discount":0,

"filledQuantity":0,

"id":30325712346546177,

"identifier":"00700",

"latestPrice":385.8,

"latestTime":1680266023000,

"limitPrice":320,

"liquidation":false,

"market":"HK",

"name":"腾讯控股",

"ocaGroupId":87055,

"openTime":1680266023000,

"orderId":92,

"orderType":"LMT",

"outsideRth":true,

"parentId":30325712346546176,

"realizedPnl":0,

"remark":"",

"secType":"STK",

"source":"OpenApi",

"status":"Initial",

"symbol":"00700",

"timeInForce":"DAY",

"totalQuantity":100,

"updateTime":1680266023000,

"userMark":"test_bracket"

},

{

"account":"13810712",

"action":"SELL",

"algoStrategy":"STP_LMT",

"attrDesc":"",

"auxPrice":280,

"avgFillPrice":0,

"canCancel":true,

"canModify":true,

"commission":0,

"currency":"HKD",

"discount":0,

"filledQuantity":0,

"id":30325712346677248,

"identifier":"00700",

"latestPrice":385.8,

"latestTime":1680266023000,

"limitPrice":278,

"liquidation":false,

"market":"HK",

"name":"腾讯控股",

"ocaGroupId":87055,

"openTime":1680266023000,

"orderId":93,

"orderType":"STP_LMT",

"outsideRth":true,

"parentId":30325712346546176,

"realizedPnl":0,

"remark":"",

"secType":"STK",

"source":"OpenApi",

"status":"Initial",

"symbol":"00700",

"timeInForce":"DAY",

"totalQuantity":100,

"updateTime":1680266023000,

"userMark":"test_bracket"

}

]

}